Social Media

Why GST was extremely important for economy like India

Goods and Services Tax (GST) rolled out as soon the clock chimed midnight on Saturday, July 1, 2017, the One Nation – One Tax – One Market, is the biggest tax reform in Indian history that promises to change the way India does business and has potential to add up to 2 percent to India’s GDP. GST that subsumes around 17 central and state indirect taxes looks set to unlock India’s latent growth potential, is expected to boost compliance, curb tax evasion and give the much needed impetus to Indian economy. Tax reforms, which have been 17 years in the making, started by Atal Bihari Vajpayee, pursued by Man Mohan Singh, and now brought to fruition by Narendra Modi, aim to simplify India’s byzantine taxation system by harmonizing country’s state and central government revenue-raising mechanisms. India’s GST is the first value-added tax to work entirely on an information technology and communications infrastructure.

GST is defined as the tax levied when a consumer buys a good or service. It is a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as services. GST has been commonly accepted by world and more than 140 countries have acknowledged the same. Generally the GST ranges between 15%- 20% in most of the countries

GST was extremely important for economy like India to rid the consumer of cascading tax effect wherein a consumer had to bear the load of tax on tax and inflationary prices. Prior to implementation of GST; Goods in India were taxed by State governments & Central Sales Tax was levied only in the case of inter-state sales, Services were taxed by the Central government which also levied a welter of excise and customs duties, surcharges, and cesses, that bogged business owners down in tedious paperwork and drove them toward black market suppliers to escape the complicated and expensive work of tax compliance. For businesses to trade across 135 crore consumers’ market, fragmented multiple taxation and interstate checkpoints created obstacles and delayed deliveries by many hours besides confiscations due to local tax rules. GST by subsuming multiple indirect taxes including central sales tax, purchase tax, excise duty, luxury tax, entertainment tax, entry tax, taxes on advertisements, lotteries, betting & gambling, service tax, additional customs duty, surcharges, state-level value-added tax and octroi; is expected to hit hard the flourishing informal economy in which less than a crore enterprises – out of more than six crore enterprises paid taxes in India.

GST was also important as it would be difficult to evade tax after its implementation, as till now paying taxes voluntarily was considered an act of stupidity and tax evasion was a normal way of conducting business. Economic greatness of a country cannot be built on such weak moral foundations and unethical business practices. India has underperformed, for decades, in comparison to other developing economies, growing at an average rate of 3.7 percent between 1950 and 1970. Japan and South Korea grew at 10 and 5 times that rate respectively during the same period.

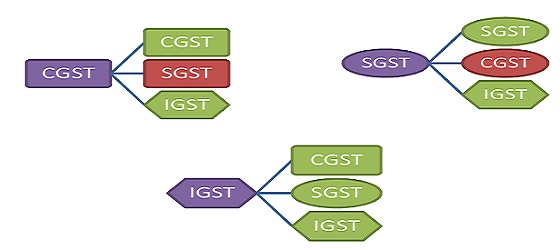

Remedy to multiple taxes and its cascading effect, a burden on common man, is GST. GST has a federal structure with three kinds of taxes namely CGST – Central, SGST – State and one called IGST – integrated GST that will help to tackle inter-state transactions. IGST will be combination of CGST and SGST and the same will be collected by the Centre in the Origin State. Under GST all forms of supply of goods and services like transfer, sale, barter, exchange and rental will have a CGST and SGST. The impact of cascading taxes can be explained with an example: Say A sells goods to B after charging sales tax, and then B re-sells those goods to C after charging sales tax. In this case while B was computing its sales tax liability, it also included the sales tax paid on previous purchase, which is how it becomes a tax on tax. This is where the need for GST arises to do away with the phenomenon.

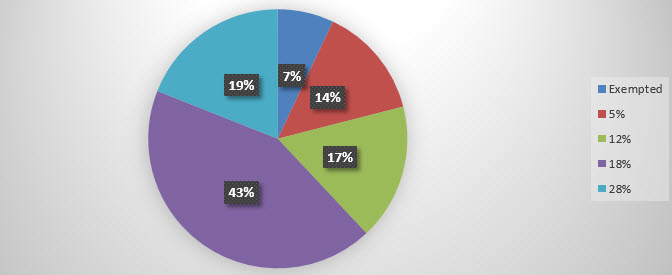

GST Council decided the rate slabs for the Goods and Services to be taxed under the GST regime. The threshold limit for exemption from levy of GST is Rs 20 lakh for the States, except for the special category where it is Rs 10 Lakh. The Council has adopted a four slab tax rate structure of 5%, 12%, 18% and 28% for GST.

Impact of GST on Indian economy:

- GST removes the cascading tax effect by merging all levies on goods and services into one, replacing a plethora of indirect taxes which contributed to bulk of revenues of the States and just about half of the tax kitty of around Rs 16 lakh crore collected by the Centre.

- Direct taxes like income tax concern only a small fraction of the population, the indirect taxes affect every Indian as they are charged on consumption, affecting both the rich and the poor. By ending multi-layered indirect tax regime, GST is expected to benefit all sections of Indian society.

- Earlier taxes like excise and central sales tax were levied on manufacturing at the factory gate or on inter-state movement of goods. Under GST, goods would be taxed at the destination. This would result in gains for the consuming state and loss for the manufacturing state. However, GST law provides for compensating the losses made by states for the initial few years.

- GST is expected to affect prices of services which earlier attracted an average service tax of around 14 per cent only at the Central level. But at the same time, the prices of several other goods are expected to decrease. Manufacturers or traders would not have to include taxes as a part of their cost of production, which would lead to reduction in prices. Experts believe that GST would serve as an anti-dote to inflation and be friendly to all stakeholders — people, industry and traders.

- The poor have been completely insulated from any adverse impact of GST. All the food and non-food items consumed by the poor have been pegged at 0% or 5% tax slab. GST will surely benefit these sections and will mean more money in their pockets.

- GST would result in fall in tax incidence for consumers – lower transaction cost for final consumers. From the consumers’ point of view, the advantage would be in terms of a reduction in the overall tax burden on goods, which is currently estimated at 25%-30%.

- GST speeds up economic union of India and will end market distortions as India has become a single market. India has more than 30 markets which would be transformed into a single market with GST.

- Fiscal barriers between states stand dismantled to stitch together a common market. Long lines of trucks waiting at check posts to cross state boundaries, a symbol of a fragmented economic architecture which encouraged corruption now stand eliminated. With most of the states removing the major trade obstacle immediately after rollout of the GST, the ease of doing business would go up significantly and operational efficiency would improve.

- Even as GST seeks to benefit everyone, its biggest impact will be felt by businesses, especially those engaged in buying or selling of goods from or into other states.

- GST will help producers sell more goods, who sometimes find it difficult to sell their products to distributors or wholesalers in other states because of a difference in tax rates and cumbersome movement of goods.

- GST aims to build a complete chain of tax payments at each stage of sale, due to its value-added taxation nature. This will lead to a huge reduction in tax evasion.

- Under GST regime, all transactions and processes required to be done only through electronic mode. This will help in minimising the physical interaction of taxpayers with tax officials. This will also help reduce tax-related corruption.

- The GST law provides transitional provisions for ensuring smooth transition of existing taxpayers to GST regime, credit for available stocks, etc.

- Some other provisions include a system of GST Compliance Rating.

- Anti-profiteering provisions for protection of consumer rights have also been included in the Acts.

- GST acquires a very simple and transparent character that would lead to ease of doing business; triggering increased economic activity and job creation while reducing corruption and tax evasion greatly.

- GST is a landmark step as it has the potential to catalyse changes in many other areas. One of the benefits is expected to be a favourable environment for Indian manufacturing and ‘Make in India’, taking the country on the path to industrialisation.

- As industrialisation is a pre-condition to absorb surplus from the struggling rural economy, it is the way India’s farm crisis can really be resolved.

- GST will be a big boon to farmers as all essential agricultural commodities have been put in 0% tax bracket.

- GST is an effective tax system that encourages compliance which is likely to result in higher revenues for governments and expected to widen the tax base. It will accelerate economic growth over the next few years and contribute to better employment opportunities.

- GST would bring improvement in cost competitiveness of goods and services in the international market. GST’s successful implementation has given a strong signal to the foreign investors about India’s ability to support business.

- Macroeconomic impact of a change to the introduction of the GST is significant in terms of effects on growth, price, current account and budget deficit.

- In a fast developing open economy with a high and growing service sector, a change in the tax mix from income to consumption-based taxes is likely to provide a fruitful source of revenue.

- Lower compliance and procedural cost: There would be reduction in the load to maintain compliance. Also keeping record of CGST, SGST and IGST separately would not be required.

- Impacts the administrative component of compliance cost of GST as well as likely increases in tax revenue from the informal, underground or black economy. This parallel informal economy that accounts for over one-fifth of our GDP will be brought into the tax network. This will yield substantially higher revenues to governments and make scarce resources available for public spending.

According to Ministry of Finance, “GST will make India a common market with common tax rates and procedures and remove economic barriers.” In the GST regime, exports will be zero-rated in entirety. This is unlike the past system where refund of some of the taxes did not take place due to fragmented nature of indirect taxes between the Centre and the States.

Arvind Subramanian, Chief Economic Adviser to the Government of India and Hasmukh Adhia, Revenue Secretary stated on Jul 19, 2016 that the country will benefit immensely in three ways from the GST:

First, the GST will greatly increase the revenues available at the states’ and centre’s disposal by expanding the tax base. More importantly, the resources of the poorer states (or consumer states) like, Uttar Pradesh, Bihar and Madhya Pradesh will increase substantially.

Second, the GST will facilitate ‘Make in India’ by converting the geographical landscape of the country into a single market. Despite being one country, India is a union of 30 or more markets. GST would get rid of the CST and subsume most of the other taxes. And since, it will also be applicable on imports, the major tax factor working against ‘make in India’ will disappear, greatly boosting the production and in turn exports. This will ultimately help bridge the current account deficit.

Third, the GST would improve tax governance in two ways:

- Like the value added tax (VAT), it is a self-collecting and self-enforcing tax. What it essentially means is that the companies buying supplies from outside parties will insist on tax payment on goods supplied as without this they can’t get setoffs on their own final product sales.

- Due to the dual monitoring structure of the GST – one by the states and another by the Centre – it is difficult to evade tax. Even if one set of tax authorities overlooks or fails to detect evasion, there is the possibility that the other overseeing authority may not.

According to Confederation of Indian Industry (CII) President Shobana Kamineni GST will make India Inc. more competitive, it will incentivise exports, help expand the tax net, contribute to the ease of doing business and accelerate new business ventures. “Input tax credit will curb inflation by avoiding tax-on-tax. We believe that most businesses would pass on the benefits of input tax credit to consumers so that inflation would be curbed.”

The day after Goods and Services Tax (GST) was rolled out; there was one development which brought cheer to consumers. Firms in sectors such as automobiles, electronics and consumer goods announced a reduction in prices of some products. This is no surprise and very much an anticipated benefit of the roll out. One of the aims of GST was to remove the cascading impact of multiple taxes which was a feature of India’s erstwhile fragmented domestic market. With the creation of a common market, some prices of some products have been marked down as the cascading impact of taxes has been eliminated.

GST is another milestone in India’s reform journey that is undoubtedly India’s biggest piece of economic reforms and has also been the most complex reform to achieve: it called for the Constitution’s division of the tax base between the Centre and the states to be amended, calling for virtual political consensus across the federal divide and the political spectrum. It took a combined effort by India’s political parties to set aside narrow interests in the pursuit of greater common good to bring about this reform. However, switching over to GST should not be seen as an end in itself. Instead it should be seen as the beginning of a process of reform to truly unshackle the Indian economy. India has a long way to go, before poverty and ignorance and disease are banished and people set free to realise their potential.

Related Articles

-

Apr 27, 2017 10:08 am

Apr 27, 2017 10:08 am

Related Articles

-

Created at: Jan 22, 2020

-

Created at: Nov 2, 2019

-

Created at: May 29, 2019

-

Created at: May 28, 2019

-

Created at: May 28, 2019

-

Created at: May 27, 2019

-

Created at: May 27, 2019